At some point over the past year, the financial media’s inflation coverage transitioned from, “Will this high inflation persist?” to, “Here’s how to cope with inflation that’s here to stay!” It seems some investors have resigned themselves to a new normal of high inflation following decades of below-average consumer price changes. However, financial market data tells a different story, one of potentially softening inflation.

Breakeven inflation (BEI) rates offer a window into the market’s inflation expectations. Defined as the difference between yields on nominal and inflation-protected bonds of the same maturity, BEI represents the inflation rate at which investors would be indifferent between the two. If actual inflation were to exceed BEI rates, investors would be better off with the inflation-protected bond; if inflation were less than BEI, the reverse would be true. BEI is therefore commonly interpreted as the average annual inflation rate expected over a given time horizon.1

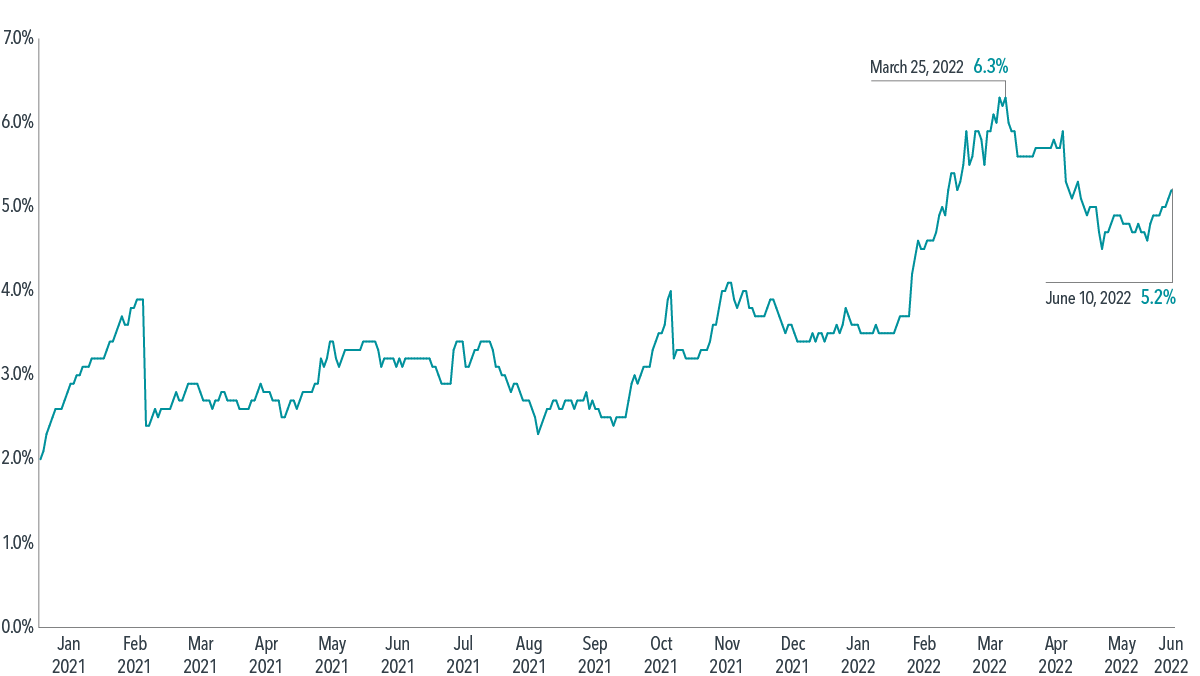

The one-year BEI shows a spike in inflation expectations this year following increasingly high consumer price index (CPI) changes. But the trajectory appears to have changed course over the past couple months (see Exhibit 1). Since peaking at 6.3% in late March, the one-year BEI had fallen to 5.2% as of June 10. This might be the market’s way of telling us it sees inflation getting under control in the near future.

Brighter Horizons

1-year breakeven inflation rate, January 1, 2021–June 10, 2022

It is important to remember that realized inflation can diverge from expectations. For example, the one-year BEI rate as of May 3, 2021, was just 2.7%. Over the next 12 months, CPI grew by 8.3%, meaning a substantial portion of this inflation seemed to have been unexpected by the market. From January 2007 to April 2022, the difference between actual inflation and that “predicted” by BEI varied from –5.59 to 8.43 percentage points.2

While nominal (i.e., not inflation-protected) bond prices reflect expected inflation, investors who opt for Treasury Inflation-Protected Securities (TIPS) or approaches that overlay inflation swaps (“real return” bond strategies) get compensated for actual inflation. Investors who want to reduce uncertainty in the event of higher-than-expected inflation may benefit from these inflation-hedging approaches.

Written by Wes Crill, PhD Head of Investment Strategies and Vice President

Dimensional Fund Advisors LP

Learn more about Monica.

Learn more about Monica.

I am a creative CERTIFIED FINANCIAL PLANNER® professional providing financial planning & tax strategies for clients by accurately assessing each client’s present and future needs, objectives, and lifelong goals. My empathetic and engaging personality helps guide clients through retirement as they discuss all of life’s complexities; focusing on specific tax strategies and evidence-based investment philosophy to meet every client’s unique goals and circumstances.

I am a creative CERTIFIED FINANCIAL PLANNER® professional providing financial planning & tax strategies for clients by accurately assessing each client’s present and future needs, objectives, and lifelong goals. My empathetic and engaging personality helps guide clients through retirement as they discuss all of life’s complexities; focusing on specific tax strategies and evidence-based investment philosophy to meet every client’s unique goals and circumstances. During my salad days, I studied business at the University of Minnesota and the Carlson School of Management. Taking this route seemed to make sense when I graduated high school, as it offered the opportunity to pursue a career in business. However, the experience didn’t go as planned. I found myself disillusioned by the focus and teachings of business school, with many of the lessons revolving around detached relationships focused solely on profit. I eventually concluded that this was not my personal path. I chose instead to purse a passion – writing – and veered off into journalism for the next six years of my life.

During my salad days, I studied business at the University of Minnesota and the Carlson School of Management. Taking this route seemed to make sense when I graduated high school, as it offered the opportunity to pursue a career in business. However, the experience didn’t go as planned. I found myself disillusioned by the focus and teachings of business school, with many of the lessons revolving around detached relationships focused solely on profit. I eventually concluded that this was not my personal path. I chose instead to purse a passion – writing – and veered off into journalism for the next six years of my life.

Pingback: androxal online

Pingback: ordering enclomiphene uk buy over counter

Pingback: cheap rifaximin canadian pharmacy

Pingback: buy cheap xifaxan buy online uk

Pingback: staxyn no prescriptions needed cod

Pingback: how to order avodart price prescription

Pingback: dutasteride online discount

Pingback: order flexeril cyclobenzaprine canada mail order

Pingback: buying gabapentin uk no prescription

Pingback: comprar kamagra original

Pingback: how to order fildena generic for sale

Pingback: buy cheap itraconazole usa where to buy

Pingback: obecný kamagra bez lékařského předpisu

Pingback: zyloprim 300 mg price

Pingback: vibramycin for uti

Pingback: esomeprazole magnesium 20 mg price

Pingback: cialis lowest price

Pingback: avanafil online canada

Pingback: vardenafil 20mg duration

Pingback: is tadalafil otc

Pingback: wellbutrin bupropion side effects reddit

Pingback: minoxidil costco shampoo

Pingback: terbinafine dosage for onychomycosis

Pingback: toradol pharmacokinetics

Pingback: avanafil contraindication clinical notes

Pingback: avanafil secure buying guidance

Pingback: vardenafil mechanism breakdown